Insurance Digital Transformation: Embracing Change

10.25.2023

The term "digital transformation" has become a buzzword across various sectors, and the insurance industry is no exception. In an era marked by rapid technological advancement, the insurance industry, traditionally seen as slow to adapt, finds itself at a crossroads. The question that looms large is whether this age-old industry is truly embracing change or still resisting innovation. Here, we'll explore the dynamics of digital transformation in the insurance sector to understand where it stands in this transformative journey.

The Case for Digital Transformation

1. Customer Expectations

Consumers can expect anything from food delivery to transportation to online shopping available at the click of a button, raising the bar for quick and convenient service across the board. Policyholders now demand seamless online experiences, 24 hours a day, for purchasing, managing, and filing claims for insurance policies.

2. Data and Analytics

The insurance industry relies heavily on data. With advancements in big data analytics and AI, insurers can harness data to improve risk assessment, pricing, and fraud detection. Embracing digital tools can make this process more efficient and accurate. This is particularly important with the cost of data breaches at a 15% increase over 3 years.

3. Competitive Landscape

Insurtech startups have entered the scene, disrupting traditional insurers with innovative business models and technology-driven solutions. Deloitte has estimated $16.5 million in investments in InsurTech startups in the last decade. To stay competitive, established insurers are being compelled to adapt and adopt similar technologies.

4. Regulatory Changes

Regulations in the insurance industry are evolving to accommodate digital innovations. Insurers must comply with these changes, which can often be easier with modernized systems and technologies, particularly since consumers do not have the patience for this traditionally slow-moving industry.

In this dynamic landscape, insurance companies face a pressing need to align with evolving customer expectations, leverage data-driven insights, and adapt to a changing competitive landscape while navigating shifting regulatory requirements. Consumers, accustomed to the convenience of seamless digital experiences in various sectors, now expect the same level of ease and accessibility when it comes to their insurance needs. With data breaches on the rise, the importance of harnessing data and analytics, facilitated by advancements in AI and big data technologies, cannot be overstated. These tools not only enhance risk assessment, pricing, and fraud detection but also contribute to operational efficiency and accuracy. Furthermore, the disruptive influence of InsurTech startups, backed by substantial investments, is prompting traditional insurers to explore and adopt similar technologies to maintain competitiveness. In the midst of these changes, staying compliant with evolving regulations becomes more manageable through the adoption of modernized systems and technologies, ultimately helping insurers meet the heightened expectations of today's impatient consumers while securing their data in an increasingly digital world.

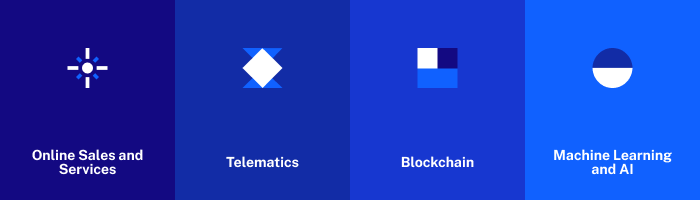

Embracing Digital Transformation

Many insurance companies are actively embracing digital transformation and making significant strides in modernizing their operations. Here are some ways in which they are doing so:

1. Online Sales and Services

Insurers are offering digital platforms for customers to browse, compare, and purchase policies. These platforms often include chatbots and virtual agents to assist customers with inquiries and claims, and many customers will be able to access policies within minutes, without going to an office or even speaking to an agent.

2. Telematics

The use of telematics and IoT devices is revolutionizing the auto insurance sector. Insurers can collect real-time data on policyholders' driving behavior using on-board diagnostics and GPS technology, enabling personalized pricing and risk assessment.

3. Blockchain

Some insurance companies are exploring blockchain technology to enhance transparency and security in claims processing and underwriting. Blockchain technology can also enable companies to detect fraud more efficiently and help users access claims much more quickly, which can be particularly important as claims for health and life insurance are often filed in times of distress.

4. Machine Learning and AI

Insurers are using AI and machine learning algorithms to automate underwriting, predict claims, and detect fraudulent activity more effectively. Insurance companies are finding AI to be particularly impactful when implemented for superior customer support.

As the insurance industry adapts to the demands of the digital age, innovative technologies are reshaping the way insurers interact with customers and manage their operations. Online sales and services have become a hallmark of the industry's transformation, offering customers the convenience of browsing, comparing, and purchasing policies at their fingertips. With the integration of chatbots and virtual agents, insurers are now equipped to provide swift assistance to customers, addressing inquiries and claims efficiently.

This digital approach not only streamlines the process but also eliminates the need for customers to visit physical offices or engage with agents directly, reducing friction in policy acquisition. Telematics and IoT devices are another game-changer, especially in auto insurance. Real-time data collection on driving behavior through onboard diagnostics and GPS technology enables insurers to tailor pricing and assess risks with precision, fostering a more personalized and fair insurance experience. Machine learning, AI, and blockchain technology round out the transformation, empowering insurers to automate underwriting, predict claims, and detect fraud with unprecedented accuracy. The impact of these technologies extends to superior customer support, redefining how insurers serve their clientele in an increasingly digital and data-driven landscape.

Resisting Innovation

While there is momentum toward digital transformation, challenges remain, and some segments of the insurance industry may still be resisting innovation. Here are some reasons for this resistance:

1. Legacy Systems

Many insurance companies still rely on outdated legacy systems that are difficult and expensive to replace. Transitioning to new technologies can be a lengthy and complex process.

2. Cultural Barriers

Resistance to change can be deeply ingrained in the culture of traditional insurance companies. Employees may be resistant to adopting new technologies and processes.

3. Security Concerns

With the increasing reliance on digital platforms, cybersecurity becomes a paramount concern. Some insurers may be hesitant to fully embrace digital transformation due to worries about data breaches and other security risks.

4. Costs

Implementing digital transformation initiatives can be costly, and some insurers may be hesitant to invest in new technologies without a clear return on investment.

Insurance companies must not resist innovation because doing so can jeopardize their long-term competitiveness and relevance in a rapidly evolving marketplace. Legacy systems, while challenging to replace, can become a hindrance to efficiency, customer satisfaction, and staying competitive. Cultural barriers, while deeply ingrained, can be overcome through effective change management strategies that empower employees to embrace new technologies and processes, fostering a culture of innovation. Security concerns, though valid, can be addressed through robust cybersecurity measures and practices that can be more secure than traditional paper-based processes. The initial costs of implementing digital transformation initiatives may seem daunting, but the long-term benefits in terms of improved operational efficiency, customer engagement, and risk management far outweigh these investments, ensuring the sustainability and growth of insurance companies in a digital age where adaptability and agility are paramount.

Evolving with the Digital Age

The insurance industry is undoubtedly in the midst of a digital transformation, with many companies making significant strides in embracing change and innovation. Ultimately, the successful digital transformation of the insurance industry will depend on a combination of factors, including regulatory support, customer demand, and the ability of insurers to navigate the complexities of this evolving landscape. As technology continues to advance and customer expectations evolve, insurance companies that resist innovation may find it increasingly difficult to compete in the modern marketplace. Embracing digital transformation is not just an option but a necessity for the insurance industry to thrive in the digital age.